Listen now

.svg)

As VCs, we have the privilege of witnessing how entrepreneurial energy combined with technology talent is solving problems in traditional industries. One area that has experienced especially rapid development is the logistics & supply chain industry.

This is why we are very happy to start 2020 by announcing a $22M Series B investment in Shippeo. Shippeo provides an end-to-end, real-time supply chain visibility platform allowing shippers or 3rd-party/4th-party logistics service providers (3/4PLs) to gain access to predictive and real-time location and estimated-time-of-arrival (ETA) information. Shippeo tracks deliveries over multiple modalities including full truckloads, less-than truckloads, parcels, and ocean cargos. With improved visibility as a starting point, their vision is to make supply chains run on their own.

Founders, Pierre Khoury (co-founder & CEO) and Lucien Besse (co-founder & COO) came up with the idea for the company in 2014 while reviewing the supply chain industry at a private equity fund. Observing an industry facing many challenges, including inefficiency, fragmentation, and lack of transparency, they decided to start a company to address these issues.

Since industry structure and dynamics play such a key role in understanding the attractiveness of Shippeo’s position in the logistics & supply chain market, we’re using the lens of industry analysis to open the door to understanding the reasons behind this particular investment.

A complex industry structure

At NGP Capital, we love to debate the implications of industry structure on the performance of our portfolio companies and investment prospects. Industry structure (i.e., the number, size, and relationships of the companies within a particular industry) gives clues to the power balance of market participants and the competitive forces brewing within an industry. This is particularly true for long-standing, stable industries that have evolved over hundreds or even thousands of years.

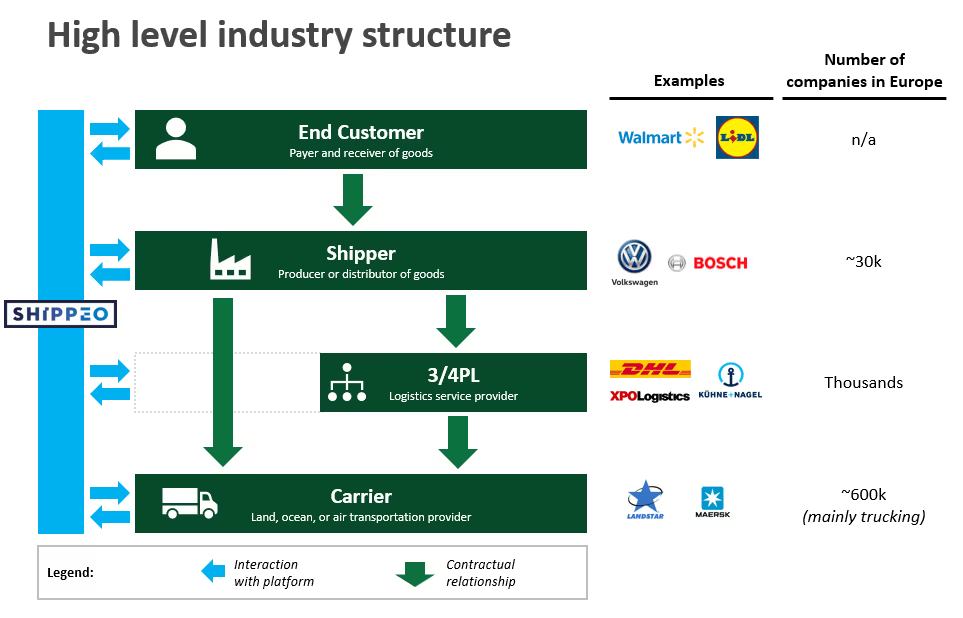

The logistics & supply chain industry is enormous, with many types of participants. Figure 2 describes the industry structure and key participants from Shippeo’s perspective, showing the various interactions and relationships among the participants. All of the participants interact with the Shippeo platform, but Shippeo’s customer is typically either a shipper or a 3/4PL.

Two key industry challenges

As a result of the complexity related to supply chains, the industry faces two key challenges:

1. Massive and persistent fragmentation

The logistics & supply chain industry is incredibly fragmented. In Europe alone, there are approximately 600,000 road freight companies, the top 20 of which own only 12% of market share.

Industries remain fragmented for many reasons, but typically the cause is the inability of companies to create economies of scale (or the presence of diseconomies of scale). In the logistics industry, having larger trucking fleets does not seem to improve customer service or increase efficiency. Why is this the case even though the logistics & supply chain industry has had thousands of years to evolve? We believe there are a couple of key reasons.

First, the logistical flows within companies are intricate and multi-dimensional, which makes optimization difficult. For example, each shipper has a unique geographic footprint of production sites and customer locations. And the type of goods transported imposes specific demands on the supply chain – for example, certain types of groceries are perishable, and bulk goods such as chemicals may require special vehicles for transportation.

Second, the industry is a technology laggard. The use of simple technologies such as digital document handling, location tracking, fleet management, and machine learning can help create economies of scale by reducing the need for back-office staff, improving routing, and increasing capacity utilization. The larger the company, the more leverage these technologies can provide. But companies in this industry are slow to adopt new technologies.

As investors, fragmentation in a particular market always piques our interest, because it usually comes with opportunities for disruption.

2. Lack of transparency

The other key issue in this market is a lack of transparency. This is largely a side effect of fragmentation and is sustained by the low technology penetration in the industry overall.

Consider this – you can track a $10 pizza in real-time with a precise ETA, but a large manufacturer often has only a +/- one-day visibility into when a truck containing millions of dollars worth of goods will arrive.

Usually, the only way to know the whereabouts of the goods en route is reactive – by calling or emailing the carrier. This not only adds considerable operational cost but more importantly, it leads to poor customer service and low customer satisfaction. The issue is exacerbated by multiple levels of subcontracting, which means that the lack of transparency and the associated increase in cost, compounds throughout the supply chain – the shipper calls the 3PL, who calls the carrier company, who then calls the subcontracted carrier, and so on.

The issue boils down to a lack of standardization in the industry. Every day, enterprise shippers rely on hundreds of small carrier companies to transport their goods. And even though many trucks today are enabled with telematics systems or other means of tracking, accessing that data in real-time and in an automated way requires building and maintaining integrations with the various systems used by the carriers. With hundreds of different carrier transportation management systems (including legacy software studded with customizations), telematics systems, and IoT solutions providing location and other data, it makes little sense for an enterprise to spend their resources building integrations with all of these different systems.

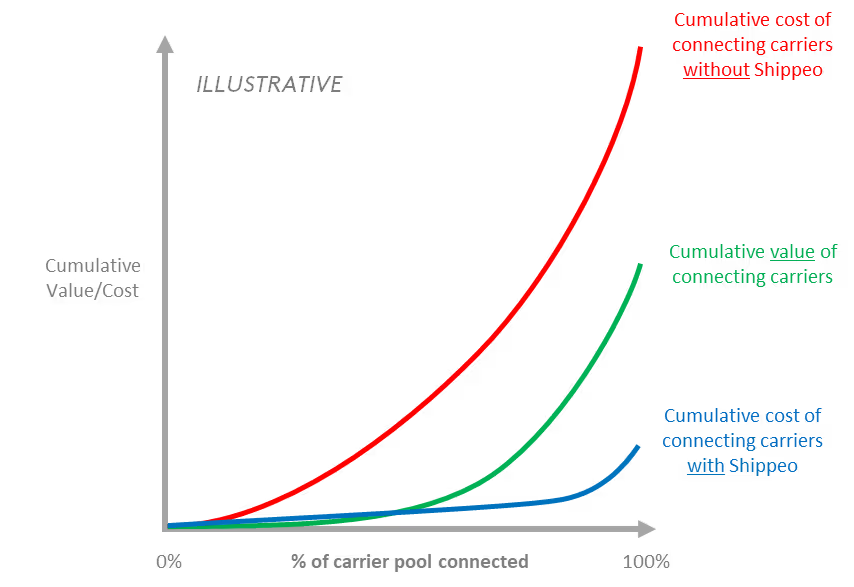

There is a fundamental incentive trap preventing development. For an individual carrier or freight forwarder contemplating offering visibility data to their shipper customers, the return on investment remains low as long as they are the only carrier offering it. The marginal benefit for a shipper of connecting with only one carrier out of fifty or a hundred is very small, so shippers are generally not willing to pay for the visibility data. At the same time, the shippers themselves are not able to consolidate visibility data across their entire carrier pool due to the extent of the effort that would be required.

Visibility data starts providing significant value only when most carriers are connected, which then unlocks opportunities to optimize or revamp supply chain processes and reap the benefits from the increased visibility.

How Shippeo solves fragmentation and transparency issues

Shippeo connects to shipper or 3/4PL transportation management systems (TMS), carrier TMSs, carrier telematics systems, and other data tracking systems (see Figure 3). By creating an overarching data and analytics layer, Shippeo creates value for all of the participants in the industry.

With Shippeo, shippers are not forced to connect to each carrier individually but hit the ground running by leveraging the more than 140,000 carrier connections that the company has built so far. Not only does Shippeo provide the data, but they also provide a communication and alerts platform to help the parties interact if problems arise, as well as analytics and insights that leverage the data across all of the carriers that Shippeo tracks. Building integrations into carrier systems is time-consuming, but once it is done, the data from that carrier can be used for multiple shippers. Thus, the value of the platform grows exponentially with scale.

Building a sustainable competitive advantage

Building a successful company is not only about being able to develop a product that solves a customer’s problem but also about how well the company can sustain its (leading) position. While Shippeo is still early in its development, our view is that Shippeo has a very attractive position in the logistics & supply chain market and can create strong barriers to entry in two key ways.

1. Network effects

Unlike many consumer-facing industries, such as social networking (e.g., Facebook), or eCommerce (e.g., Amazon), the potential to create network effects tends to be quite rare in the enterprise software business. When we first met with Shippeo, we became very excited about the huge potential to build a moat around their business through network effects.

As Shippeo adds more carriers to its platform, it becomes faster and cheaper to integrate new shippers. At the same time, as Shippeo tracks more and more transports, it grows its data asset, which enables better optimization and automation of the supply chain (e.g., improved ETA calculations) for all of their customers.

Network-effect businesses are tough to get off the ground, but once they’ve reached a critical mass, they become almost unstoppable. We believe Shippeo has reached this inflection point by having connected to hundreds of transportation management and telematics systems, and more than 140,000 carriers, serving more than 50 enterprise customers and growing their revenues by more than 300% last year. From a competitive perspective, what all this means is a strong deterrent to the entry of other players in this market.

2. Deep integration and switching costs

Shippeo strives to become a long-term partner to its customers and integrates deeply into their processes in order to provide as much value as possible. By understanding the key pain points of their customers, and by growing with their customers, Shippeo is earning their customers’ trust. As validation of their approach, Shippeo experienced a 0% customer churn rate in 2019. Shippeo is proving to be much stickier than many other enterprise software products.

Putting it all together

The logistics & supply chain industry, shaped over a long period of time, has yet to consolidate due to the difficulty of creating economies of scale in an industry with thousands of participants using hundreds of different systems. In addition, the lack of transparency in an industry with low technology penetration means that a considerable amount of resources is being wasted.

Shippeo is building an automation layer that connects these fragmented pieces of the supply chain. As its data asset grows through more integrations, Shippeo can not only help to optimize the internal operations of individual companies, but can bring predictive insights, reduce downtime, and enable collaboration across the industry.

Together with new investors ETF Partners and Bpifrance, and existing investors Partech, Frst, and SAP.io, we are looking forward to supporting Pierre Khoury, Lucien Besse, and the team at Shippeo on their journey to automate supply chains.

Please feel free to reach out at ossi@ngpcap.com in case you have comments/feedback on the post or wish to exchange thoughts on the industry.

Related articles

Interview with David Tang by AllChinaTech

Lime raises another $310 million, bringing its valuation to $2.4 billion

Recruiting tips for the scaleup phase – Shippeo’s 4 key steps to hiring well during fast growth