Listen now

.svg)

The future is finally here with 114 global, commercial deployments of 5G. By 2024, 5G is expected to handle 25% of all mobile traffic data. 5G brings innovation and flexibility at the radio layer, democratizing access to ultra-fast connectivity and data-intensive applications. However, to understand the implications of 5G, we need to understand Edge Cloud, an essential co-traveler technology required to make widespread adoption of 5G a reality.

The exponential growth of devices and the data generated from them creates the need for an entirely new architecture to process data in an effective way. The first wave of cloud computing was about hyper-scale centralized processing. The new wave of cloud computing is about processing at, or close to, the scene of data generation. Federation is the name of the game. Between a speedy, smart, often private edge and a fully amortized public cloud that has set the software standard for developers to quickly adopt new technology.

The Market Opportunity

Centralized public cloud computing reduced the cost of experimentation for software companies and enabled software-as-a-service (SaaS) business models. In addition to the $100B per year spend on the cloud itself, the public cloud has given rise to a slew of digital-native businesses, which are valued at $150B/year. Traditional verticals like manufacturing, retail, logistics, and healthcare, though, have latency-sensitive use cases, which require hardware/software deep tech solutions.

The digitization of these verticals, which are still mostly untouched by the centralized public cloud, creates a market opportunity on the order of trillions of dollars. Gartner estimates that by 2025, 75% of the meaningful data generated will be outside the organization's perimeter. Edge infrastructure will make it economical to process the data at, or close to, the scene of data generation and make it easier for developers to create new edge native applications, transforming these verticals.

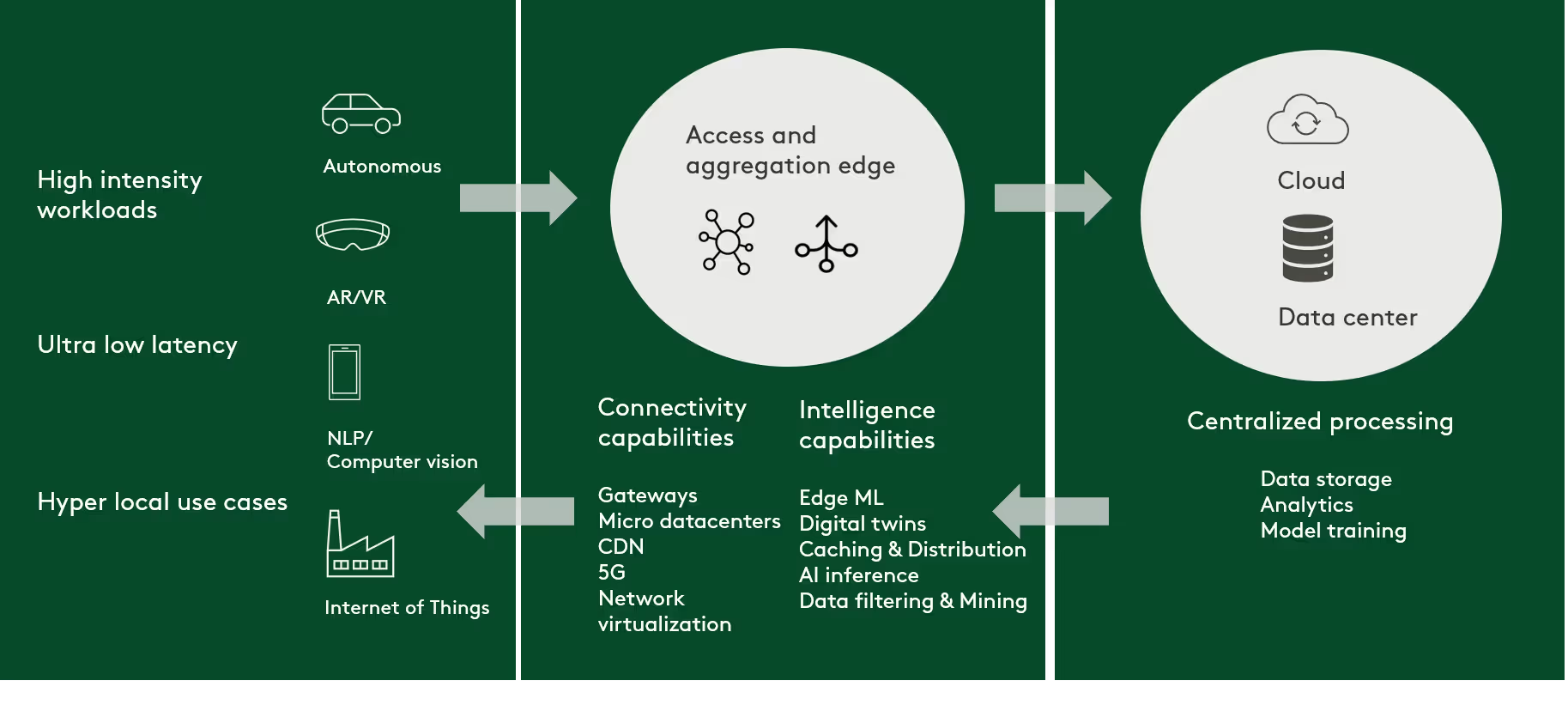

The Landscape

Edge Cloud includes several layers of technology that come together to satisfy high intensity, low latency workloads, which form the basis of edge use cases. The edge infrastructure consists of Device Edge (sensors, wearables, chips, connected cars, factory robots etc. at the scene of data generation); the Access and Aggregation Edge (compute and AI infrastructure to run connectivity and intelligence workloads close to the scene of data generation), and Centralized Processing (where private/public clouds provide the abstraction layers needed for developers to create intelligent applications).

The edge cloud landscape can be segmented as follows:

- Edge Hardware – Primarily driven by AI chips, edge hardware has seen some interesting innovation and funding activities in recent years. There is an ongoing debate on whether the innovation needs to happen at the silicon layer or by optimizing the software stack. Either way, we view innovations at the chip level as the strongest signal of what we can expect up the tech stack.

- Edge AI – Democratization of AI models has created tools and platforms that enable running AI inference and training at the edge.

- Edge Connectivity – These include modern networking solutions like SD-WAN, programmable CDNs, ORANs etc. which aim to decouple hardware from the software thus reducing CAPEX and increasing the adoption of cloud/edge native networking solutions.

- Real-time data – These include tools that are reinventing the analytics stack and driving real-time data processing at the edge.

- Edge Compute – Compute at the edge requires managing highly distributed infrastructure paving the way for interesting solutions that enable deployment, orchestration, observability at the edge.

The gold lining

Public cloud growth has been driven by a compelling cost advantage and a uniform software stack, both of which benefited from unprecedented standardization. The edge promises to be more unruly both because of the enormous variety of clients beyond PCs and smartphones and because of immovable constraints that require intelligence and processing at the edge. Three laws – the laws of physics, the laws of economics and the laws of the land especially around data governance – are driving the move of computing, storage, network and security infrastructure into the access and aggregation edge. These three laws also create unique opportunities for entrepreneurs to work with.

Constrained by the laws of physics and latency requirements, we see opportunities for entrepreneurs to strike strategic partnerships with traditional infrastructure providers like data centers, co-location providers, network operators and telco equipment providers to leverage their preexisting immovable assets to create unique software ecosystems.

Constrained by the laws of economics around data transmission, we see real-time data processing and AI at the edge really taking off. Opensource solutions will drive experimentation and enterprise adoption at the edge and traditional enterprises will warm up to developer lead adoption rather than top-down sales motion.

Lastly, constrained by the laws of the land, data privacy, and edge security will no longer be an afterthought when designing edge applications and use cases. This creates a unique opportunity for entrepreneurs in the security and data privacy space to adapt existing solutions or craft brand new solutions for the edge.

Our bet is that Edge Cloud and its capabilities will serve as the breeding ground for new use cases and strong business models. At NGP Capital, we are eager to partner with entrepreneurs building the next generation of Edge Cloud companies. If this sounds like you, please reach out.

Here are the fastest-growing companies in Edge Cloud, as quantified by Q, NGP Capital's AI-driven platform, which scans and ranks more than 700,000 companies around the world in the fund's chosen investment areas every week:

Related articles

The secret to keeping a large global business agile

Indix closes $15 M in Series B Funding

VC Journal: The rise of unicorns – a funding event, not a destination