Listen now

.svg)

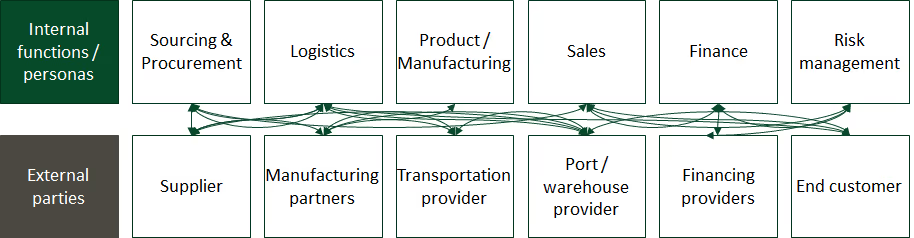

A worst-case example is mass recalls – a scenario that can deteriorate both brand equity and cash flows for months or even quarters after the procurement decision. The below chart illustrates the complexity of supply chains as well as the transparency and collaboration requirements that organizations face in building resilience and managing cost.

Chart I: Illustrative supply chain overview

More than $5 billion is spent annually on procurement software, and the category is growing at 12% annually. Coupa, a spend management platform founded in 2006, manages over $2 trillion of annual spend. IDC reported that Coupa generated $220M in procurement software revenues last year with 27% growth. Yet Coupa is the number three player, with a 4% market share. SAP and Oracle control one-third of procurement software spend.

Given the scale of procurement spending, incremental improvements can have a meaningful impact on cash flow and profit margins. Procurement is highly strategic for many companies, especially for companies with physical products.

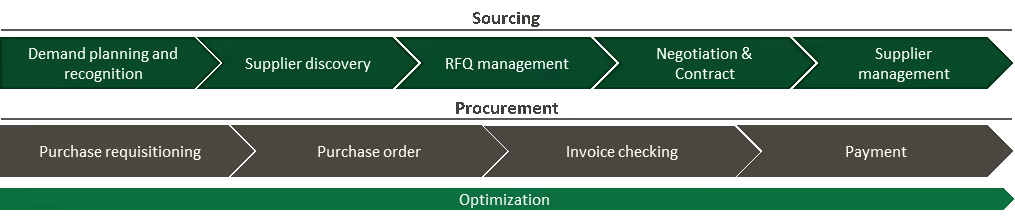

Procurement can be split into two broad categories: Sourcing and Procurement. Sourcing starts with identifying requirements and discovering suppliers, then moves on to selection, closing, and managing the supplier relationships. Procurement is more process-driven and repetitive in nature, and includes tasks ranging from purchase requests to invoice management and payments. Analytics and spend optimization apply to both categories.

Chart II: High-level source-to-payment flow

The strategic nature of spend categories is driven by multiple factors. Product-related categories are highly strategic and are defined as direct procurement. This means that the choice of suppliers and contracts will impact everything from gross margin to inventory levels, product quality, and brand equity. Spend categories like travel and logistics are defined as indirect procurement. While travel and logistics are not directly part of the end product, these are typically large spend categories, which increases the importance of optimization. Logistics, as previously explained, is also a key enabler for unlocking competitive advantage throughout the supply chain. Some spend, like office equipment, is not strategic, but nevertheless must be monitored from a cost optimization perspective.

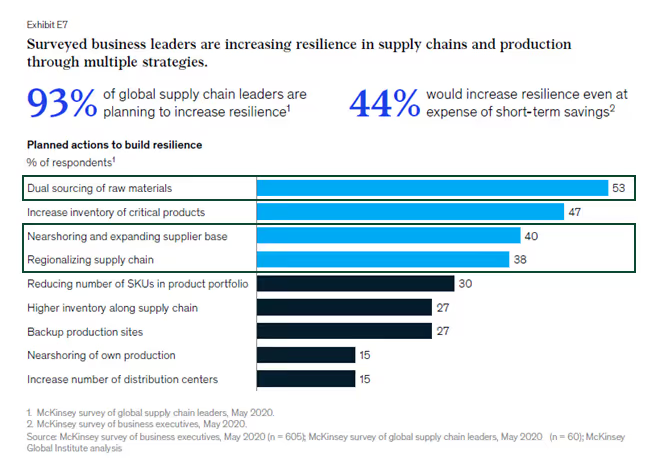

The strategic nature of sourcing is demonstrated in a recent McKinsey report on supply chain resilience. The report cites sourcing-related actions as three of the top five actions that can increase supply chain resilience.

Chart III: Planned actions for building supply chain resilience

The topic of supply chain management and resilience has gained increased attention due to the dual shocks of the COVID-19 pandemic and US-China trade tensions. These shocks are on top of longer-term trends such as rising demand volatility, ESG requirements, and shortened lead times. Complex global supply chains must now re-evaluate their sourcing strategies. We believe categories that include planning, optimization, automation, discovery, and collaboration are ripe for disruption.

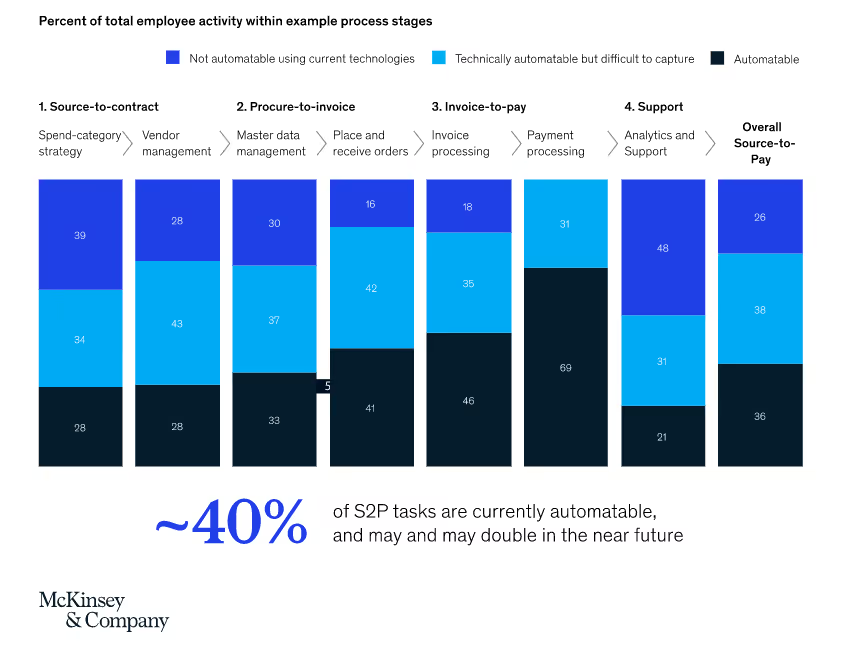

McKinsey estimates that ~40% of procurement tasks, from spend strategy and planning to payments and analytics, can be automated with currently available technologies. BCG predicts that digital solutions can reduce the end-to-end time for procurement processes by up to 80% for standardized items like office supplies and by 40% for more complex items like capital spend. The combined improvements could generate savings of 1% to 3%.

Chart IV: Automation potential of procurement

The opportunities in sourcing and procurement have yielded significant venture-backed outcomes, including market leaders Ariba (acquired by SAP) and Coupa (trading at a $17 billion market cap). However, we believe that the field is open for best-of-breed solutions to accelerate growth in the category, empowering procurement teams with the required tools for the complexities of today. Why?

1. Market leaders like Coupa and Ariba do not solve all customer problems.

2. Management consultants remain widely used for procurement projects.

3. There is a prevalence of in-house tools.

4. The potential of AI remains largely unleveraged.

5. We see strong momentum for companies like Globality, Keelvar, Scoutbee, and Sirion.

With supply chain shocks from both trade wars and the pandemic, sourcing and procurement are likely to gain further attention in boardrooms as enterprises continue to invest in real-time, end-to-end supply chain management. This past week, Coupa announced the acquisition of Llamasoft for $1.5 billion, a timely reminder of the demand for data-first approaches to supply chain design. Enterprises cannot afford relationship-first supply chain processes. New solutions are emerging that use machine learning to establish a competitive advantage through procurement and supply chain management.

A new crop of companies is emerging, and we expect more activity in the procurement space going forward as momentum builds.

Related articles

TechCrunch: SoftBank-backed Getaround acquires Norwegian car rental startup for $12M

VC Journal: Contrarian investing in venture capital today

Part 2: Exploring the business value of 5G