Listen now

.svg)

Restructuring the enterprise sector – the new focus of the China economy

The population in China is currently about 1.4 billion, a bit more than the combined population of the US and Europe of 1.1 billion. In the consumer sector of China’s economy, Baidu, Tencent, and Alibaba combine for a market cap of $0.7 trillion, closing in on the $1.5 trillion market cap represented by the combination of Google, Facebook, and Amazon. However, the enterprise sector of the China economy has fallen far behind. China has almost the same number of enterprises – 20 million compared to 25 million in the US and Europe – but of those, only a handful have market caps over $10 billion, and an even smaller minority are in the $4-5 billion range. Compare this to the combination of Oracle, SAP, and Salesforce, which together represent a market cap of $370 billion.

Source: National Bureau of Statistics, Wind, McKinsey Global Institute

China’s consumer sector has historically outpaced its enterprise counterpart due to the country’s double-digit GDP growth and a focus on top-line acceleration. Now that GDP growth has slowed, the focus has shifted.

Restructuring the enterprise sector is the new focus of the Chinese economy. Targeting cost savings and efficiency improvements, enterprises are beginning to seek increased profits rather than just growth. In addition, enterprises will need to deal with fundamental changes in the labor market, a long-standing advantage of the local economy. Sourcing employees will no longer primarily be a matter of costs as a new generation enters the workforce looking for more fulfilling jobs than those of the past.

The digital transformation of China’s enterprise sector

A lack of digitalization produces a “bullwhip effect” on supply chains, where small fluctuations in customer demand can cause progressively larger fluctuations in demand at the distributor and manufacturer levels. Digitalization creates new synergies that can alleviate these problems. Instead of a linear model, where a small change at one end causes increasingly larger problems as you move down the chain, digitalization of the supply chain turns it into a reticulated model. This network of interconnected nodes creates new synergies among stakeholders that can improve the stability and financial performance of an entire industry.

Evaluating enterprise software opportunities

China is finding its own, unique way to reshape its enterprise sector. New, emerging solutions will combine cloud-based software and data infrastructure with an increasingly digitalized supply chain that features new user behaviors, organizational structures, and channels. For example, leaders in aftermarket solutions (e.g., CarZone and Mancando) might concentrate on new channels, SaaS, and data infrastructure, while industrial solutions (e.g., Zhenkunxing) might depend primarily on building new organizational structures, data infrastructure, and electronics component solutions such as ICBase (SZSE: 300184, $1.3B Market Cap).

Enterprise software differs from its US counterparts primarily in terms of monetization and the maturity of its economics. Large, recurring revenue streams are common in the US, while in China, monetization comes from down the supply chain, as many enterprise software companies rely on commissions from transactions to make up software revenue. For example, US-based Intuit Inc. derives most of its revenue from its online and desktop products, while the China-based Hui Suan Zhang monetizes by directly providing services to SMBs and collecting service revenue, as well as by licensing its software to franchises and taking a revenue cut as a license fee.

Cloud services in China (SaaS, IaaS, PaaS)

The US is well into the cloud era, with over 90% of enterprise software solutions incorporating at least some cloud elements. Top players in the US market, Salesforce (CRM) and Workday (Finance, HR), with revenues of $13 billion and $2.8 billion respectively, have sustained revenue growth of 30-35% YoY. In contrast, 45% of enterprise software in China includes no cloud capabilities at all. The top enterprise software players in China, Yonyou (ERP/CRM), and Neusoft (Manufacturing) have revenues of $1.2 billion each, and growth is relatively slow.

The cloud services market in China is currently less than 10% of the US cloud services market, but is changing quickly across all sectors:

- Cloud Infrastructure is the largest and fastest-growing segment, representing over 60% of the cloud services market and growing at 82% annually.

- IaaS/PaaS is a $5 billion market in China with local players (Alibaba, Tencent, Huawei) leading the competitive charge.

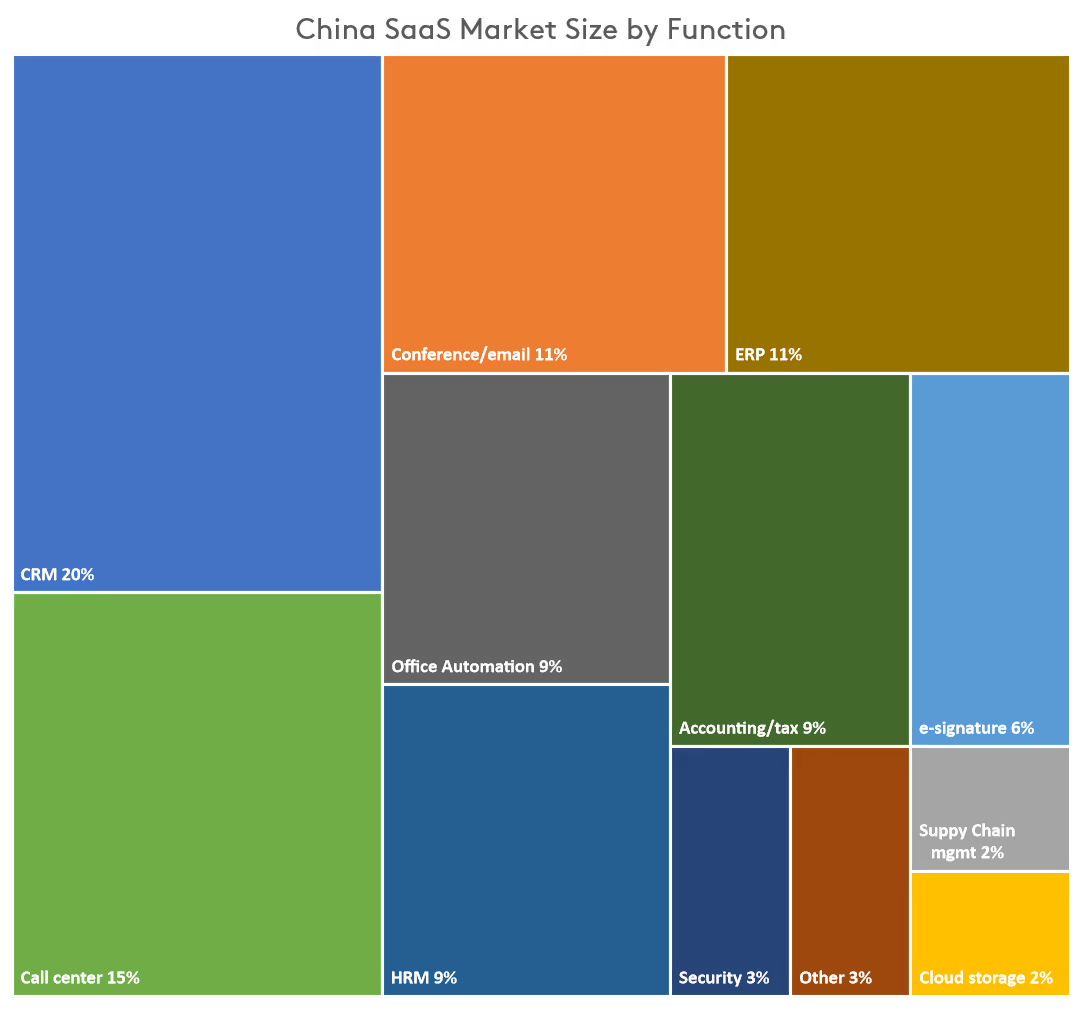

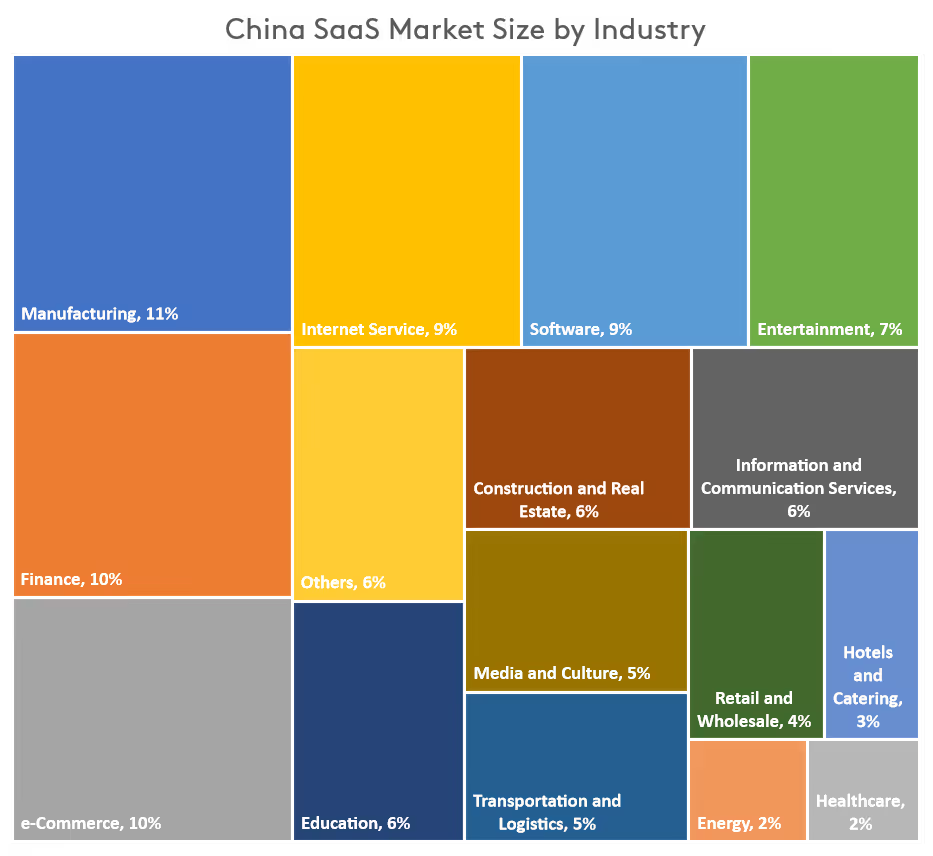

- SaaS is less than one-third of the cloud services market in China today, but is growing at 40%, nearly twice the rate of the global SaaS market. While this market is considerably more fragmented (no company owns more than 5% market share), similar functions as those in the US/EU have emerged in the graphs below.

Source: iResearch, Alibaba Cloud Research, CNITEYES

The rise of China’s enterprise economy

As China shifts its focus to the enterprise, the next generation of software will drive corporate efficiencies and digital transformation. In much the same way consumer tech created giants such as Alibaba, Tencent, and ByteDance, we expect similar companies to rise to the top in the enterprise market.

Related articles

Unlocking the value of voice technology

Kubernetes Podcast with Platform9

Scandit Raises $30M in Series B Led by GV to Bring the Internet of Things to Everyday Objects Through Computer Vision and Augmented Reality