Listen now

.svg)

As of May 1, 30 million US workers have filed for unemployment. Supply chains have been disrupted – farmers are destroying produce even as food banks see unprecedented lines. Our transit infrastructure saw usage and ridership plummet. The repercussions from COVID-19 have been unlike any other event in history.

However, there are signs of life. Wuhan emerged from lockdown in early April. European nations are lifting travel restrictions and US states are reopening in the coming weeks.

While much remains unclear on how the COVID-19 crisis will evolve, we believe the fundamental case for smart mobility remains intact. The virus has exposed weaknesses in our transportation and logistics infrastructure that smart mobility seeks to address.

Pre-COVID Slowdown

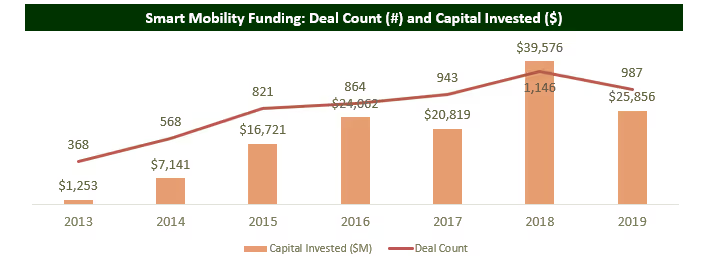

Prior to 2019, growth-oriented investors funneled $25 billion into Uber and Lyft. Over 70 different LIDAR and sensor companies raised venture rounds. Valuations for logistics companies mirrored high margin SaaS businesses. Between 2013 and 2018 venture funding for smart mobility grew 31x.

But smart mobility funding declined 35% in 2019 while deal volume fell 14%. The markets adjusted as public market investors called on companies to focus on profitability and unit economics rather than growth. Leading smart mobility companies have costs while others have quietly folded or been acquired.

During Covid

The lockdowns announced in March have taxed transit, traffic, and logistics supply chains. For companies moving people and freight, the fallout exacerbates the slowdown that started in 2019.

The decline in transportation traffic is unprecedented in the past century. By early April, US air traffic declined 96%, public transport usage dropped to almost zero and a fraction of people were on the roads. Moovit has captured transit data over 130 countries and the trends are similar globally.

Ridesharing and micro-mobility companies are directly impacted. Uber and Lyft suspended carpooling and reports indicate that rides are down 70% in cities under lockdown. Lyft recommended that its drivers seek delivery gigs with Amazon to stay busy. After exiting a few cities in 2019, Lime suspended scooter service in nearly all markets. Bird shut all its European markets and several in the US and laid off one-third of its workforce. These shutdowns occurred even as cities deem shared scooters and bikes essential services.

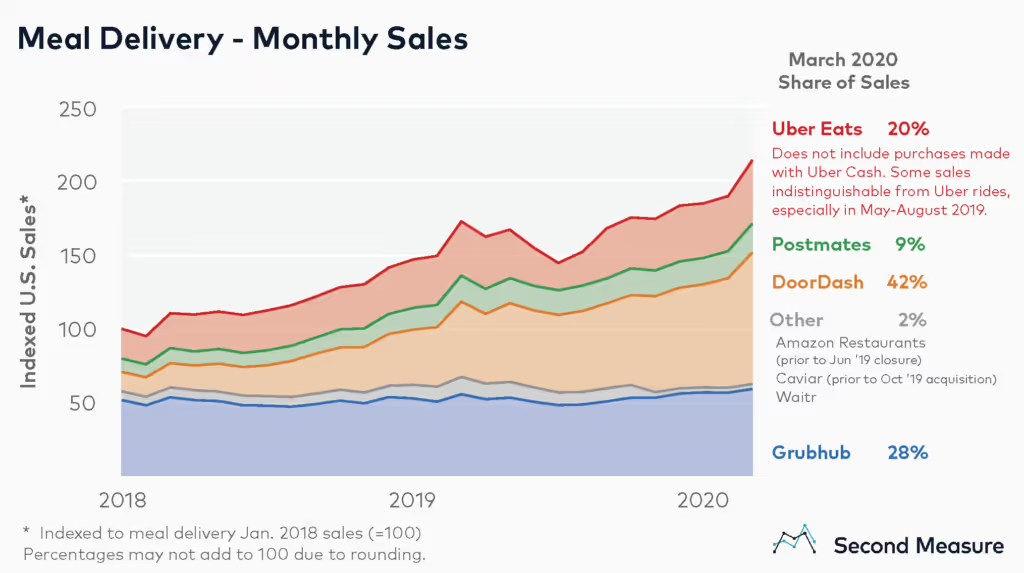

Ecommerce and home delivery demand surged inversely with a decline in transportation. 3PLs are experiencing holiday-like demand, straining supply chains. In his annual letter to shareholders earlier this quarter, Jeff Bezos announced Amazon plans to hire 175,000 workers for its warehouse and fulfillment teams. Second Measure data shows a 24% year over year increase in meal delivery services at the end of March. Food delivery – previously considered a convenience – is now part of normal (lockdown) life.

Post COVID-19 Landscape

It is likely to take years to return to normalcy and COVID-19 will cause some permanent changes in work paradigms and commute behaviors. As Mark de la Vergne, Chief of Mobility Innovation for the City of Detroit said, “It will take at least a decade for Detroit to return to levels of transport service that we had pre-COVID given new safety and fiscal considerations.”

Based on our discussions with transportation experts, city planners, and our portfolio companies, following is our 2020 view on forthcoming changes in commute patterns in the years ahead.

- Unlocking Lockdowns: The lockdown started abruptly. The release will be more complicated and gradual. In China, bikeshare players saw ridership decline over 50% during the lockdown as riders stayed at home but returned to 75% of normal as people return to work gradually.

A new normal is emerging around remote work. Zoom saw usership grow 30x and top 300 million users in the past three months. Much digital work can be done remotely. Employees and employers may agree to extend work from home even when lockdowns are lifted. On site employment in many companies will never return to pre-COVID levels. This is a boon for employees who will spend less time commuting with reduced congestion and more remote work options. Mobility companies will need to redesign their systems to provide equal quality of service and profitability with lower commute volumes. - Safety is Job #1: Employers and transit providers must make commuter safety a top priority. Employer responsibility for employee welfare is no longer just within the confines of the office; it now extends to commute to and from the office. Transit providers will need to redesign their systems considering both biological as well as physical safety. Public transit usage will decline substantially. Taxi and ride hailing companies must retrofit their cars and practices to reduce risk of virus transmission. Micro-mobility and carpooling systems must assure safety.

- Shift in Consumer Behavior: Crises are a catalyst for change. After the SARS outbreak, eBike sales exploded in China, growing 250x to 10 million by 2005 from 40,000 in 1998. Consumers sought alternatives to crowded public transit a pattern repeated in New York City at the start of the COVID-19 pandemic. New York Times reported that CitiBike saw a 67% increase in ridership as commuters avoided the subway.

Rideshare, micro-mobility, and on-demand delivery uncovered significant consumer demand prior to COVID-19. The pandemic could solidify consumer use on these new services as consumers look for safer ways to accomplish city trips and receive goods. - Autonomous and Electric Vehicles: The fundamentals for a shift to alternative, shared vehicles is intact. Consumer willingness to use autonomous vehicles may increase long term as they offer safer, cheaper transportation alternatives. But autonomous and electric vehicles will suffer a several year setback as the crises and recession reduce corporate investment, consumer propensity for new capital purchases and regulatory initiatives in this area.

- Consolidation: COVID-19 brings a set fresh of challenges to mobility companies, however the sentiment shifted on the sector before the outbreak. The space was consolidating and forcing companies to prove whether profitable businesses could be built. The economic turmoil will accelerate the wave of consolidation, leaving fewer firms to in the post-virus landscape. Companies that are well-capitalized and can survive stand to benefit from less competition and efficiency gains from operating larger networks. This is already happening. Bird acquired Circ. Lime acquired Boosted Boards. Grow Mobility was acquired for $1 by a Baidu subsidiary after raising over $200M from venture investors.

As governments initiated rapid lockdowns mobility companies responded in kind: quickly adjusting business models and adapting to a new normal in transportation. Reduced usage and tighter capital markets will accelerate a day of reckoning for some. Others will stand to thrive in the post-virus economy. The gradual return to normal economic life will necessitate new behaviors and safety measures in how people move around – and mobility companies that accommodate these changes.

Read part 2: Logistics in the COVID Era

Subscribe to our monthly Smart Mobility Newsletter

Related articles

Navigating the growth round in today's economy

Building an effective board

Empowering Manufacturing with Autonomous Robots: Why We Invested in Ati Motors