Listen now

.svg)

At NGP Capital, we have invested in industrial tech startups for seven years across categories like worker augmentation (Scandit), robotics interoperability (SVT Robotics), and supply chain optimization (Shippeo, Spacefill). A topic that is often up for discussion is the scalability of industrial tech, especially in the context of venture capital.

Over the years, we have met with hundreds of industrial tech companies. We’ve observed that industrial tech at the early stages often doesn’t scale as well as SaaS for business applications, but when it does, there tend to be strong moats that lay the foundation for fundamentally durable businesses.

Earlier this year we put our heads together with our advisor and industry executive Guido Jouret (former CDO of ABB) to structure a framework of factors that we believe foster scalability in industrial tech. The framework follows a product market fit structure which guides us as investors to form a view of how a specific company manages typical scalability hurdles in industrial tech. The items that we have included in the framework do not represent an exhaustive list, but based on our experience, even the most successful companies rarely tick all the boxes. More importantly, we believe that VC-backed companies need a clear strategy and execution plan in terms of overcoming the typical hurdles; be it sales velocity, implementation times, or interoperability. Even if the hurdles have not yet been overcome, we find it very compelling when an entrepreneur clearly articulates the hurdles and why and how the company will mitigate them.

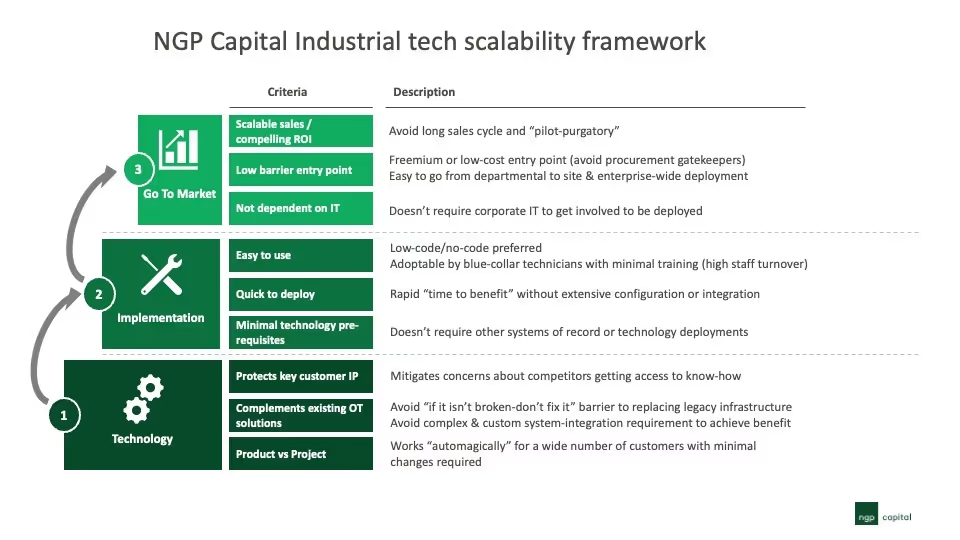

We’ve broken our framework into three main buckets:

1) Technology scalability

The key factor that we look for is the level of product standardization vs customization requirements. If each customer comes with material customization requirements, we typically need to know how the company intends to abstract itself from the customization project while maintaining control of the customer experience and go to market velocity. Our portfolio company Scandit, which provides enterprise grade computer vision technology across industry verticals is a great example of a company that has overcome the customization trap. They partner extensively with key players in their ecosystems such as hardware vendors and system integrators, allowing the company to focus on the product instead of projects.

Second, while we certainly appreciate companies building from the ground up, we are conscious that industrial buyers are sensitive to the uptime of their facilities and processes. As a result, companies that can work with existing infrastructure tend to have better fundamentals for fast growth vs companies that end up replacing a lot of customer infrastructure.

2) Implementation scalability

Companies that rely on the customer implementing third-party products or technologies in parallel to unlock the full value of the product usually raise a significant market timing question. We usually view these situations as indications of an early market where we need to build a lot of conviction around the segment-specific market timing. The more equipped a company is to work with the limitations of the customer, the better.

Focusing on empowering a wide enough share of the customer organization through e.g. a no-code first approach is something that we actively look for as it can lessen the dependency on IT buy-in or the need to tap into developer resources which tends to be a scarce asset. Tulip is a great example of a company that allows for fast implementation and low-friction customization through a modular and no-code product strategy.

Our portfolio company Shippeo built its network of integrations from the ground up. As Shippeo added more carriers to its platform, it became faster and cheaper to integrate new shippers by which they increasingly overcame the “Quick to deploy” obstacle. At the same time, as Shippeo tracks more and more transports, it grows its data asset, which enables better optimization and automation of the supply chain for all of their customers. Seeing network effects like these in play is critical for integration centric products.

3) Go To Market scalability

Industrial customers tend to be closely managed by existing vendors with whom relationships can date back decades. Startups also run a high risk of getting sucked into lengthy procurement and PoC processes. Demonstrating GTM scalability proof points is usually a key hurdle to overcome for Series A and B stage companies.

While chasing the next multimillion ACV deal with a blue-chip customer can sound attractive, we think that starting small and demonstrating the product value is the better way to go. Of course, all companies do not have the ability to do so due to technology or unit economics limitations. Companies that can drive a product-led growth like GTM motion for industrials in parallel to direct sales is something that excites us a lot. Given the fragmented nature of the industrial market, we are also intrigued by companies that can sell to the mid-market as these buyers often require more complex abstraction compared to enterprise customers which brings us full circle to the product vs project question.

Samsara is one of the most successful industrial tech companies with an arguably unprecedented scaling journey in industrial tech with their ARR exploding from $20M in FY2018 to $194M in FY2020. We believe that this journey would not have been possible without solving each of the scalability hurdles listed in our framework.

If a company doesn’t tick the boxes in our framework, it doesn’t mean that we would not consider an investment. Most investments that we make are far from ticking all the boxes, but absent of a clear playbook to overcome these typical hurdles, it does have implications for growth potential. With growth being the main value driver in VC, it will impact the ability to fundraise.

Hopefully, this framework provides useful guidance in terms of what we look for regardless of the market segment within industrial tech. We also recognize that seven years in the market is early days, and we very much welcome challenging views and comments. And if you’re an industrial tech startup in Europe or US, reach out to us here.

Image credit: Shane Rounce

{kind=link}

Related articles

Part 2: Logistics in the COVID Era

Decoding the VC Code: How investor reputation affects startup fate

Adaptable AI for Manufacturing – Why We Invested in GrayMatter Robotics